Transitioning into retirement often requires shifting from a mindset of accumulation to one of strategic decumulation, where a single financial decision can dictate the quality of life for decades. For many American retirees, the prospect of securing a guaranteed lifetime income through a $1 million immediate annuity seems like the ultimate safety net, providing a level of certainty that the volatile stock market cannot match. However, the initial appeal of a high monthly payout can mask a significant structural vulnerability that endangers the financial stability of a surviving spouse. While a single-life payout might provide an impressive monthly check of over $6,100, this figure is predicated on the lifespan of only one individual. If that person passes away shortly after the contract begins, the entire principal balance typically vanishes, leaving the surviving partner with a massive income void. This catastrophic loss of cash flow, occurring precisely when medical bills peak, illustrates why yield is rarely the safest choice for survival.

The Trade-off Between Yield and Liquidity

Comparing a $1 million investment into an immediate annuity against the current performance of government bonds reveals a stark contrast in potential returns. As of 2026, a 10-year Treasury note may offer a stable but modest 4% yield, whereas an annuity can frequently push that annual distribution figure toward 7% or higher by utilizing mortality credits. These credits are essentially the pooled funds of annuitants who pass away earlier than expected, which the insurance company then redistributes to those who live longer. While this mechanism allows for a higher stream of income than traditional fixed-income instruments, it comes at the steep cost of total irrevocability. Once the contract is signed and the premium is paid, that $1 million is no longer a liquid asset that can be accessed for unforeseen global events or family emergencies. This fundamental trade-off means that the primary value of the asset is the reliability of the payout structure selected at the start of the deal.

The total loss of liquidity inherent in immediate annuities creates a rigid financial environment that requires meticulous planning of external reserves. Because the lump sum is effectively gone, any sudden need for capital—such as major home repairs, legal fees, or advanced medical treatments—must be met by other sources of wealth. This lack of flexibility becomes particularly dangerous when a household has committed too large a percentage of its net worth to a single-life annuity product. In such scenarios, the retiree is essentially betting that their longevity will justify the loss of the principal, but this bet often ignores the reality of the spouse’s future needs. Without a significant secondary bucket of liquid cash, the surviving spouse might find themselves with a dwindling checking account and no way to tap into the $1 million that was supposed to fund their joint retirement. This represents a high-stakes gamble that often undervalues the necessity of partner liquidity.

Analyzing Payout Models and Survivor Hazards

One of the most overlooked aspects of annuity planning is the devastating interaction between single-life payouts and the loss of secondary income streams like Social Security. When one member of a married couple passes away, the household immediately loses the smaller of the two Social Security checks, which can represent a significant reduction in monthly purchasing power. If the primary earner also opted for a single-life annuity to maximize immediate income, that entire payout disappears as well, creating a double blow that can push a surviving spouse into sudden poverty. This risk is compounded by the fact that most fixed annuities do not include cost-of-living adjustments, meaning the real value of the remaining income will continue to erode over time. For a widow or widower who may live another twenty years, the combination of a vanished annuity check and a reduced Social Security benefit creates a financial chasm that is nearly impossible to bridge without outside assets.

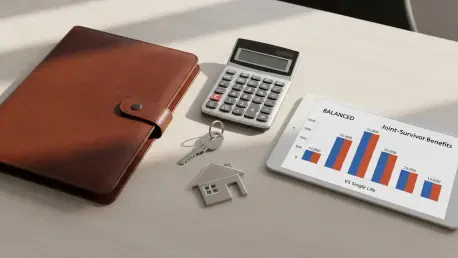

Choosing the correct payout model necessitates a cold, analytical look at long-term math rather than an emotional attachment to the largest monthly check. A single-life option provides the highest immediate return because the insurer’s liability ends when the annuitant dies, which is why it is often marketed as the most lucrative choice. In contrast, a 100% joint-and-survivor annuity might reduce the monthly income from approximately $6,100 down to $5,200, representing a noticeable decrease in current lifestyle funding. However, that $900 difference functions as a critical form of insurance, guaranteeing that the full monthly payment continues for as long as either spouse remains alive. This protection ensures that the $1 million investment serves its intended purpose as a lifelong safety net for the family unit rather than a short-term windfall. By accepting a slightly lower yield today, a couple effectively secures the surviving partner’s ability to maintain their standard of living.

Strategic Considerations for Long-Term Security

Some financial planners suggest a strategy known as pension maximization, which attempts to capture the higher yields of a single-life annuity while still providing for a spouse. This approach involves taking the largest possible annuity payout and using the surplus cash—the difference between the single-life and joint-life amounts—to pay premiums on a private permanent life insurance policy. The theoretical benefit is that the surviving spouse receives a tax-free death benefit lump sum that can be reinvested to replace the lost annuity income. However, this strategy is fraught with operational risks that can easily derail a retirement plan, including the potential for high insurance premiums based on the annuitant’s health or age. Furthermore, if the insurance policy were to lapse due to missed payments, the surviving spouse would be left with neither the annuity nor the insurance proceeds. Reliance on this complex arrangement requires a level of disciplined management over decades.

To build a truly resilient retirement, couples moved toward a holistic view of their portfolio that balanced guaranteed income with strategic liquidity and survivor protections. Financial experts increasingly determined that unless a spouse possessed an entirely independent and substantial source of wealth, the 100% joint-and-survivor option remained the most prudent default selection. It was also considered essential to maintain a cash reserve equivalent to at least two years of living expenses outside of the annuity to provide a buffer against the lack of liquidity. Consulting with a fee-only fiduciary offered a way to navigate the dense beneficiary rules and tax implications of these products without the influence of commission-based sales pressure. This proactive approach allowed families to transform a $1 million annuity from a potential liability into a durable foundation for mutual security. Ultimately, the focus shifted to ensuring the income stream remained unshakeable for both partners.