The global maritime insurance sector is currently navigating a profound structural transformation as traditional methods of risk assessment collide with the sophisticated tactics of modern deceptive shipping practices. For decades, the Automatic Identification System served as the reliable bedrock of maritime situational awareness, providing underwriters with a seemingly transparent and consistent view of vessel locations, speeds, and voyage histories. However, the recent rise of “dark activity”—a complex spectrum of deceptive practices ranging from signal jamming to identity cloning—has effectively rendered AIS-only underwriting models obsolete in the current high-stakes environment. This shift is not merely a technological update but a fundamental move toward Multi-Source Intelligence, which allows insurers to verify vessel behavior through independent, unalterable sensors rather than relying on self-reported signals that are easily manipulated.

As massive insured losses mount and the “shadow fleet” of non-compliant vessels expands, the industry is witnessing a breakdown in the predictability of historical loss models. The convergence of geopolitical instability at key maritime chokepoints and the destabilization of global trade routes has forced a total recalibration of how risk is priced and managed. Today, the ability to discern the truth behind a vessel’s digital footprint is the primary differentiator between a profitable portfolio and one exposed to terminal regulatory penalties or catastrophic physical losses. By moving toward a verification-based model, underwriters are attempting to restore a sense of order to a market that has been increasingly clouded by intentional deception and unprecedented physical risks.

Financial Implications of High-Impact Maritime Disasters

The Baltimore Bridge Collapse: A Catalyst for Market Realignment

The catastrophic collapse of the Francis Scott Key Bridge in Baltimore serves as a definitive case study for the inadequacy of legacy risk models and the dangers of underestimating modern maritime liabilities. When the incident occurred, initial market assumptions suggested that insured losses would hover around a manageable $1.5 billion, a figure that heavily informed the early pricing strategies for the 2026 reinsurance renewals. However, as the complexity of the salvage operations, business interruption claims, and infrastructure replacement costs became clearer, revised assessments placed the total loss at over $2.8 billion. This massive discrepancy sent shockwaves through the global reinsurance market, revealing that many underwriters were relying on outdated infrastructure reports and failing to account for the sheer scale and destructive potential of modern, ultra-large vessels.

This revision of loss estimates was not merely a local concern but a systemic event that consumed nearly the entire reinsurance tower of the International Group of P&I Clubs. The resulting “profitability gap” emerged because a significant portion of global marine capacity had been written against an anticipated reality that fell far short of the actual liabilities incurred. As a result, the market found itself dangerously exposed to subsequent catastrophes, with little capital buffer remaining to absorb additional high-impact events. This incident proved that historical data is an increasingly poor predictor of future outcomes when the physical assets—the ships themselves—have outpaced the capacity of the infrastructure they navigate. Consequently, underwriters have been forced to implement more rigorous stress-testing of their portfolios, moving away from average loss expectations toward a focus on maximum foreseeable loss in every major transit corridor.

Tail Risks and Infrastructure: The Impact of Vessel Scale

The Baltimore disaster also forced a fundamental reclassification of “tail risks”—those extreme, low-probability events—into what are now considered “recurring exposures” in an era of massive vessel scale. As global trade continues to rely on increasingly enormous ships to achieve economies of scale, the margin for error within aging coastal infrastructure has narrowed to almost zero. Insurers can no longer treat these bridge strikes or port blockages as once-in-a-generation anomalies when the physical dimensions of modern container ships and tankers are fundamentally incompatible with many of the world’s most critical transit points. This mismatch between vessel size and infrastructure durability has created a permanent layer of volatility that traditional underwriting models, which prioritize frequency over severity, are poorly equipped to handle.

Furthermore, the pressure on the reinsurance and retrocession markets has reached a breaking point, driving a mandatory update in how catastrophic risks are modeled and priced across the entire industry. Leading marine insurers are now incorporating granular infrastructure data, such as bridge pier protection ratings and waterway depth fluctuations, directly into their algorithmic pricing models. This proactive approach acknowledges that the safety of a voyage is no longer just about the seaworthiness of the hull but also the resilience of the environment through which it moves. By treating these massive disasters as predictable consequences of current shipping trends rather than freak accidents, underwriters are beginning to close the gap between perceived and actual risk, although this transition has led to significantly higher premiums for operators of the largest vessel classes.

Technical Failures and the Rise of Deceptive Shipping

The Breakdown of AIS: Navigating the Fog of Signal Manipulation

The most significant technical challenge currently facing underwriters is the widespread weaponization of the Automatic Identification System, which has transformed from a safety tool into a medium for deception. Originally designed for collision avoidance and short-range tracking, AIS is an unauthenticated radio system that is highly vulnerable to manipulation, yet it remains the primary data source for many compliance tools. In the early months of 2026, incidents of GPS jamming and sophisticated signal spoofing reached record highs, particularly in the Middle East and the South China Sea. Because the financial incentives for hiding a vessel’s true location now far outweigh the risks of being caught, underwriters can no longer trust that a ship is where its digital signal says it is, creating a “data vacuum” that obscures the reality of maritime movements.

This breakdown of digital trust has profound implications for risk accumulation and sanctions compliance. When a vessel manipulates its AIS data to show it is in the open ocean while it is actually loading cargo in a sanctioned port, the insurer is unknowingly exposed to severe legal and financial penalties. Moreover, the prevalence of “ghost shipping”—where a vessel disappears from the map only to reappear hundreds of miles away with a physically impossible transit history—has made it nearly impossible to maintain a clear picture of global vessel distribution. To counter this, underwriters are increasingly demanding that owners provide secondary verification of positioning through encrypted satellite tracking systems. This dual-track approach aims to strip away the anonymity provided by signal manipulation, ensuring that the contractual obligations of a policy are based on physical reality rather than a digital fabrication.

The Shadow Fleet: Managing Identity and Regulatory Exposure

The emergence of the “shadow fleet” has introduced a new level of complexity to the marine insurance market, as over 2,000 vessels are now estimated to be operating outside of traditional regulatory frameworks. These ships, primarily involved in the transport of sanctioned oil and commodities, utilize a variety of techniques to mask their identities, including frequent reflagging and the use of non-compliant registries in nations such as Nicaragua. When a vessel’s identity becomes fluid, the underwriter’s risk extends far beyond simple physical damage to the hull; it encompasses terminal regulatory exposure and the potential for a total loss of coverage should the ship be seized by authorities. This segment of the global fleet represents nearly a fifth of the total tanker trade, making it too large to ignore yet too opaque to insure through conventional means.

These shadow vessels often participate in high-risk ship-to-ship transfers in remote hotspots, away from the prying eyes of port authorities and traditional monitoring systems. Because these transfers frequently occur without proper safety oversight or environmental safeguards, the risk of a major oil spill or collision is significantly heightened. For insurers, the challenge lies in identifying when a seemingly “clean” vessel in their portfolio begins to interact with this clandestine network. Legacy compliance tools that rely on static watchlists are increasingly failing to catch these shifts, as the shadow fleet is constantly evolving and regenerating under new names and shell companies. Consequently, underwriters are shifting toward behavioral analysis, flagging vessels that exhibit “deceptive patterns” such as unusual stops or sudden changes in ownership, even if they are not currently on a formal sanctions list.

Geopolitical Volatility and Route Disruptions

Strategic Chokepoints: The Vulnerability of Global Transit Hubs

The escalation of regional conflicts has demonstrated with startling clarity how quickly a critical trade chokepoint can transform into an impassable “no-go zone” for commercial shipping. The near-total collapse of traffic through the Strait of Hormuz during recent hostilities serves as a prime example of how geopolitical events can rewrite the rules of maritime transit almost overnight. In these volatile environments, the marine insurance market effectively becomes the de facto authority on international trade, as the withdrawal of coverage or the imposition of prohibitive war-risk premiums can make it economically impossible for even the largest fleets to enter a conflict zone. This power dynamic places underwriters at the center of global supply chain stability, requiring them to make split-second decisions based on rapidly changing intelligence.

These crises trigger immediate and massive surges in war-risk premiums, which have been known to increase by sixtyfold within hours of a military escalation. Such radical price shifts reflect the extreme uncertainty inherent in modern conflict, where precision-guided munitions and drone technology can target a vessel with little to no warning. For the shipping industry, these costs are often passed down the supply chain, leading to inflationary pressures on a global scale. Underwriters must now maintain dedicated geopolitical intelligence units to monitor these hotspots in real-time, as the traditional “wait and see” approach to risk assessment is no longer viable. The goal is to identify the early warning signs of a chokepoint closure before a fleet is trapped, allowing for proactive rerouting and the preservation of capital in an increasingly unstable world.

Corridor-Based Aggregation Risk: The Cost of Global Rerouting

As vessels are systematically rerouted away from dangerous corridors like the Suez Canal, they are frequently forced to take the much longer path around the Cape of Good Hope, which adds thousands of miles and weeks of travel time to their rotations. While this strategy successfully avoids direct kinetic threats in conflict zones, it introduces a host of new problems for insurers by significantly extending the duration of exposure for every single voyage. A longer time at sea inherently increases the probability of machinery failure, heavy weather damage, and crew fatigue, all of which are covered under standard marine policies. This extension of the risk window has forced underwriters to reconsider their annual premium structures, as the “average” voyage is now considerably more hazardous than it was just a few years ago.

Furthermore, the concentration of global shipping around the southern tip of Africa has created a new phenomenon known as “corridor-based aggregation risk.” This occurs when a massive volume of insured value is funneled through a single, narrow geographical path, creating a situation where one localized event could impact a significantly larger portion of an insurer’s portfolio than previously modeled. For example, a severe weather system or a regional dispute near the Cape could simultaneously threaten hundreds of vessels, potentially leading to a concentration of claims that exceeds an insurer’s local capacity. Underwriters must now account for this geographical clustering of risk, moving away from the assumption that maritime exposure is globally distributed. This requires sophisticated spatial modeling tools that can track the real-time density of a portfolio and trigger alerts when the concentration of value in a specific corridor becomes dangerously high.

Transitioning to Multi-Source Intelligence

Synthetic Aperture Radar: Seeing Through the Darkness

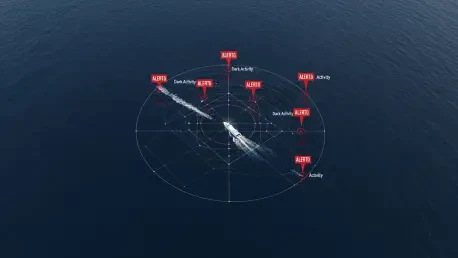

To restore visibility in an environment where AIS data is no longer reliable, the marine insurance industry is increasingly turning to advanced sensor technologies like Synthetic Aperture Radar. Unlike traditional optical cameras, which are limited by daylight and weather conditions, SAR can “see” through thick cloud cover, smoke, and total darkness by using microwave pulses to map the surface of the sea. This capability is essential for detecting “dark” vessels—those that have intentionally disabled their AIS transponders to hide their activities—allowing underwriters to maintain a continuous and objective record of maritime presence in sensitive areas. By comparing SAR detections with reported AIS positions, insurers can immediately identify discrepancies that indicate deceptive behavior or illegal ship-to-ship transfers.

Beyond simple detection, high-resolution SAR and optical satellite imagery provide a wealth of data that can be used to verify the physical characteristics of a vessel. For instance, an underwriter can use satellite data to measure a ship’s draft, which indicates whether it is empty or fully loaded, providing a crucial check against its reported cargo declarations. If a tanker claims to be in ballast but satellite imagery shows it is riding deep in the water, it is a clear indicator of a fraudulent voyage. This level of physical verification is becoming a standard requirement for high-value policies, as it provides an immutable audit trail that is immune to the signal manipulation techniques used by the shadow fleet. This transition from “reported data” to “observed data” is the cornerstone of the modern intelligence-led underwriting approach, ensuring that carriers are only insuring risks they can actually see and verify.

Artificial Intelligence: Synthesizing Global Data for Predictive Risk

The sheer volume of data generated by satellite sensors, radio frequency scanners, and global shipping registries is far beyond the capacity of human analysts to process effectively. Consequently, artificial intelligence has become the final, essential piece of the maritime intelligence puzzle, acting as a force multiplier that synthesizes billions of data points into actionable insights. AI-driven platforms are now capable of generating real-time “implausible voyage” alerts, which flag vessels whose reported paths and speeds are physically impossible according to the laws of maritime transit. By identifying these “identity inconsistencies” as they happen, underwriters can intervene before a policy is bound or a claim is paid, significantly reducing the industry’s exposure to fraud and sanctioned activity.

Moreover, AI tools are being used to develop predictive risk models that can anticipate where the next major incident or regulatory breach is likely to occur. By analyzing historical patterns of deceptive shipping and correlating them with current geopolitical trends, these systems can assign a “risk score” to every vessel in a fleet, allowing underwriters to focus their due diligence on the most suspicious assets. This proactive stance marks a departure from the traditional reactive model of insurance, where risk was only assessed after an incident occurred. Instead, the industry is moving toward a continuous, algorithmic oversight model that can detect the subtle signatures of dark activity long before they manifest as a physical loss. This technological evolution is not just about catching bad actors; it is about providing insurers with the confidence to write business in a volatile world by grounding their decisions in sophisticated, data-driven reality.

Operationalizing Modern Due Diligence

The Know Your Vessel Framework: Proactive Verification

The move toward an intelligence-led market has necessitated the operationalization of data across the entire policy lifecycle, a rigorous framework that the industry has termed “Know Your Vessel.” Much like the “Know Your Customer” protocols in the banking sector, KYV requires insurers to perform a deep-dive verification of the physical asset and its history before a policy is ever bound. This process involves cross-referencing official registry data with independent sensor histories to ensure that the ship on the insurance slip is exactly what it claims to be. By checking for historical discrepancies in vessel name, flag, and ownership, underwriters can prevent high-risk or fraudulent ships from hiding within legitimate corporate fleets, effectively filtering out bad actors at the point of entry.

This proactive verification stage is becoming increasingly automated, with insurance platforms integrating directly with maritime intelligence providers to provide a “traffic light” system for new submissions. A green light indicates a vessel with a consistent and transparent history, while a red light triggers an immediate, manual review of the ship’s recent movements and ownership changes. This streamlined approach allows underwriters to maintain high volumes of business while ensuring that every individual risk meets a minimum threshold of digital transparency. In the current market, the failure to perform this level of due diligence is no longer seen as a minor oversight but as a major operational failure that can lead to devastating financial and reputational consequences. The KYV framework has thus become the primary defense mechanism for insurers seeking to navigate the complexities of the modern maritime landscape.

Continuous Monitoring: Securing the Policy Lifecycle

The transition toward a sophisticated, intelligence-driven underwriting model was solidified as carriers recognized that maritime risk is inherently dynamic rather than static. Once a policy was bound, the industry historically moved into a passive phase, but the challenges of 2026 demonstrated that a vessel appearing compliant at renewal could engage in illicit activities just weeks later. To address this, insurers adopted continuous behavioral monitoring, which tracks a ship’s movements throughout the entire duration of the policy. This ongoing oversight allowed for the immediate detection of AIS gaps timed to known sanctions-evasion corridors or sudden, unannounced changes in management. By maintaining a persistent digital watch over their portfolios, underwriters discovered they could identify emerging threats in real-time, providing a level of security that was previously unattainable.

The integration of verified sensor data with shipping documents eventually became the gold standard for defending claims and ensuring total regulatory compliance. As the complexity of the maritime environment deepened, the carriers that succeeded were those that moved away from a declaration-based model toward one rooted in constant verification. This shift did more than just mitigate losses; it provided a blueprint for how the insurance industry could adapt to a world where the surface of the sea was no longer transparent. By leveraging Multi-Source Intelligence, the market was able to restore the trust that signal manipulation had stripped away, ensuring that maritime insurance remained a viable and stable foundation for global trade. The lessons learned during this period of high volatility provided the necessary tools for the industry to manage the risks of the future with a newfound level of precision and confidence.