Simon Glairy is a leading authority in the fintech landscape, known for his deep expertise in risk management and the institutional integration of digital assets. With years of experience guiding financial entities through the complexities of insurance and blockchain, he possesses a unique

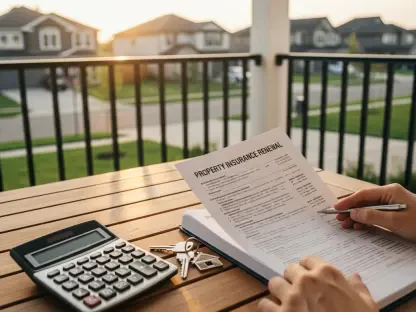

A typical homeowner opening an annual renewal notice today often finds a figure that fundamentally alters their financial outlook for the coming year. What used to be a secondary concern behind interest rates and property taxes has suddenly surged to the forefront of the American political

The current Australian corporate environment demonstrates a significant gap between the theoretical protection offered by Accident and Health (A&H) insurance and the actual recovery results seen by employees. This disparity suggests that the primary differentiator between successful and

The vibrant landscape of the Kenyan medical insurance sector presents a puzzling contradiction where explosive market growth is frequently overshadowed by deep financial instability and mounting operational deficits. While medical coverage has surged to become the dominant segment within the

For decades, the 4% withdrawal rule served as the bedrock of retirement planning, yet recent economic shifts have exposed significant vulnerabilities in this once-reliable strategy. As market volatility and inflationary pressures redefine the financial landscape in 2026, the American Enterprise

A single compromised line of code in a secondary subcontractor's server can dismantle the security perimeter of a multi-billion dollar enterprise within minutes, yet most executives still cannot name the entities that process their most sensitive data downstream. This lack of transparency

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71