The relentless volatility of extreme weather patterns in the Great Plains has long presented a formidable challenge for the traditional insurance industry, which often struggles to price policies accurately in high-risk zones. In Oklahoma, a state that endured a staggering sequence of 152 recorded tornadoes during the 2024 season, the limitations of conventional underwriting have become increasingly apparent to homeowners and regulators alike. As legacy providers pull back or implement broad, regional rate hikes that ignore specific property improvements, the entry of tech-centric firms like Kin marks a significant shift toward digital-first risk management. By leveraging machine learning and extensive geospatial datasets, these organizations aim to replace outdated actuarial models with a more granular approach. This transition represents more than just a new market entry; it serves as a critical test case for whether advanced technology can maintain insurance affordability and availability in regions most vulnerable to the intensifying effects of climate change.

Precision Underwriting in High-Risk Geographic Zones

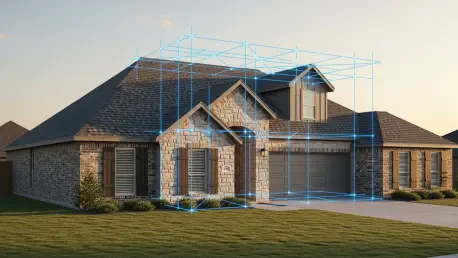

The Transition to Granular Data Analysis: Modern Modeling Techniques

The shift away from regional generalizations represents a fundamental change in how property risk is quantified in storm-prone environments. Traditional insurers typically rely on historical loss data aggregated across entire ZIP codes, which can lead to inflated premiums for homeowners who have invested in storm-resistant upgrades. In contrast, modern digital platforms utilize artificial intelligence to examine thousands of unique data points for every individual residence, ranging from roof geometry and construction materials to specific proximity to wind-shielding terrain. This high-fidelity modeling allows for a more equitable pricing structure where the cost of coverage directly reflects the physical reality of the structure rather than a broad statistical average. By integrating real-time satellite imagery and historical meteorological trends, these systems can identify properties that are statistically less likely to suffer catastrophic damage, thereby offering competitive rates in areas that were previously deemed too risky by conventional standards.

Market Competition through Technological Efficiency: Expanding Consumer Choice

Introducing advanced technological frameworks into the Oklahoma insurance landscape disrupts the existing market dynamics by providing much-needed competition in a space dominated by a few major players. The efficiency of a digital-first model significantly reduces the overhead costs associated with manual underwriting and legacy administrative systems, allowing these savings to be passed directly to the consumer. For Oklahomans, this means access to a more responsive service model that includes instant quoting capabilities and streamlined digital interfaces. Furthermore, the presence of tech-driven competitors forces traditional carriers to reconsider their own data strategies, potentially leading to a broader industry-wide modernization. As these platforms now cover more than half of the total addressable market in the United States, their expansion into volatile regions like the Midwest suggests that data-driven resilience is becoming the new standard for financial protection against natural disasters.

Resilience and Long-Term Market Stability

Automated Recovery Systems: Enhancing the Claims Process

The integration of sophisticated technology extends far beyond the initial purchase of a policy, playing a vital role in the immediate aftermath of severe weather events. When a tornado or significant hail storm occurs, digital-first insurers utilize predictive modeling to anticipate the volume and location of claims before they are even filed. By combining high-resolution aerial photography with automated damage assessment tools, companies can verify losses with unprecedented speed, often initiating the payout process within hours of the event. This rapid response is critical for homeowners who need immediate funds for temporary housing or emergency repairs to prevent further structural degradation. The synergy between high-tech efficiency and human-led support teams ensures that the claims process remains empathetic yet highly optimized, reducing the administrative friction that often exacerbates the stress of recovering from a natural disaster in high-impact regions.

Strategic Planning for Climate Volatility: Future Risk Mitigation

Homeowners in Oklahoma were encouraged to view insurance not merely as a reactive expense but as a proactive component of a broader property resilience strategy. The emergence of data-driven providers offered a clear incentive for residents to invest in reinforced roofing, impact-resistant windows, and secondary water barriers, as these improvements were finally being recognized through lower premiums. It became essential for property owners to conduct regular audits of their coverage to ensure that their policies reflected the most recent technological advancements in risk assessment. Moving forward, the industry trend shifted toward a model where constant monitoring and individual risk mitigation were the primary drivers of market stability. By embracing these innovative platforms, the local population secured more reliable protection against environmental threats, ultimately fostering a more resilient housing market that remained viable despite the persistent challenges of living in a high-risk weather corridor.