A high-stakes corporate environment where an automated agent accidentally transfers millions of dollars due to a minor logic flaw has shifted from a science fiction trope to a legitimate board-room anxiety in the mid-2020s. Corporations across the United States have integrated generative models and

Homeowners across the nation are increasingly turning to advanced surveillance technology to safeguard their properties, yet this very reliance on digital eyes can inadvertently create new vulnerabilities that traditional insurance policies were never designed to handle. As the adoption of smart

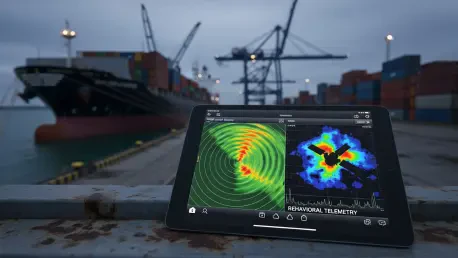

The vast, once-predictable expanses of the global oceans have transformed into a theater of structural volatility where the traditional laws of maritime transparency no longer provide a reliable safety net for insurers. By the middle of 2026, the maritime industry has reached a tipping point where

The stark reality of Nigeria’s healthcare landscape is defined by a precarious balance where a single medical emergency often translates into immediate financial catastrophe for the average household. As of 2026, health insurance enrollment remains stalled at approximately 22 million people, which

Simon Glairy has built a career at the intersection of high-stakes corporate innovation and the gritty reality of hands-on problem-solving. After years of spearheading new ventures within the structured halls of global giants like Johnson & Johnson, Procter & Gamble, and WeightWatchers, he

The landscape of corporate risk management in Mexico is currently undergoing a radical metamorphosis that has rendered traditional, manual brokerage models largely obsolete in favor of highly sophisticated, data-driven frameworks. This shift is not merely a technical upgrade but a fundamental

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87