Imagine the sudden realization that hits a homeowner when they discover a foot of standing water in their basement after a standard summer thunderstorm, only to have an insurance agent explain that their comprehensive policy provides absolutely zero financial protection for that specific event. This scenario plays out across the country with alarming frequency because many individuals operate under the dangerous assumption that the general term water damage encompasses every possible moisture-related disaster. In reality, the fine print of a standard homeowners policy creates a sharp divide between internal mechanical failures and natural external events, leaving a massive coverage gap that often remains undiscovered until a crisis occurs. Understanding the legal definitions used by insurance providers is not merely a matter of administrative curiosity but a vital necessity for financial survival. The distinction between a broken pipe and a rising river determines whether a family receives a payout for repairs or faces the prospect of paying tens of thousands of dollars out of their own savings.

The Critical Distinction: Internal Failures Versus External Flooding

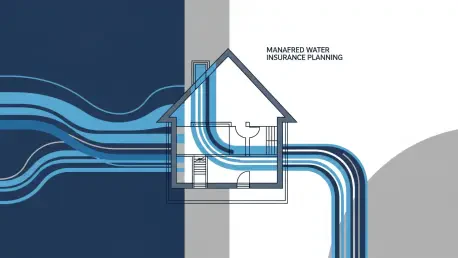

Standard homeowners insurance is specifically structured to address incidents that are classified as sudden and accidental, provided they originate from within the structure’s internal systems. When a copper pipe inside a wall corrodes and bursts or a pressurized hose leading to a washing machine suddenly snaps, the resulting deluge is typically covered because the source of the water is contained within the property’s plumbing. These events are viewed as maintenance issues or mechanical failures that fall squarely under the umbrella of basic dwelling protection. Insurance companies generally agree to pay for the drying of floors, replacement of ruined drywall, and restoration of personal property in these specific contexts because the water never touched the outside ground before entering the living space. However, the definition of accidental is strictly interpreted, meaning that slow leaks occurring over several months due to neglect are often excluded, forcing owners to maintain their systems diligently to ensure valid claims.

The legal landscape changes the moment water makes contact with the earth outside the home, as insurance providers then reclassify the event as surface water or flooding. If rain collects on a saturated lawn and eventually seeps through a foundation crack or flows over a door threshold, it is no longer considered a standard water damage claim under a basic policy. This type of intrusion falls into the category of a flood, which requires a separate policy typically backed by the National Flood Insurance Program or a specialized private carrier. This distinction is one of the most common points of contention during the claims process, as homeowners often argue that the rain caused the damage, while the insurance company argues that the ground caused the damage. Without a specific flood endorsement, residents living in even low-risk areas can find themselves entirely unprotected from the financial devastation caused by a single afternoon of intense precipitation that causes local street runoff to enter their properties.

Addressing Vulnerabilities: Infrastructure and Specialized Riders

Many property owners in established metropolitan regions face heightened risks due to the reality of aging municipal infrastructure and the increasing frequency of extreme weather patterns in the current environment. Even if a house is not located near a traditional body of water like a river or a coast, it can still experience severe flooding when city storm drains and sewer systems reach their maximum capacity. When these public systems fail to divert runoff quickly enough, the excess water has nowhere to go but into lower-level residences, often through the very drains designed to carry waste away. This phenomenon creates a unique hazard where the water entering the home is not just clean rainwater but a hazardous mixture of sewage and street debris. Standard policies almost never include protection for this type of backup, leading to a situation where a family must manage both significant property loss and a serious biological hazard without any assistance from their primary insurance provider.

To mitigate these specific risks, homeowners must proactively seek out specialized endorsements such as the Sewer and Drain Backup rider, which acts as a bridge between standard coverage and flood insurance. This specific add-on is designed to provide financial relief if a sewer line malfunctions or if a sump pump fails to operate during a power outage or mechanical breakdown. It is a critical distinction for anyone with a finished basement to understand, as the presence of a sump pump does not inherently mean that the insurance company will pay for the damage its failure might cause. In fact, many standard policies specifically exclude any damage resulting from the failure of a sump pump unless the extra rider is present and active. These endorsements are generally affordable compared to full flood insurance but offer a vital safety net for the most common ways water enters a home during a heavy storm. Evaluating these options before a storm occurs is the only way to guarantee that the basement remains a viable part of the living space.

Effective Mitigation: Strategies for Restoration and Recovery

When water intrusion occurs, the speed of the response determines whether the structure can be saved or if it will suffer from permanent issues like mold growth and structural rot. Homeowners who moved quickly to extract standing water using industrial-grade wet-dry vacuums and high-capacity dehumidifiers often saw significantly better outcomes than those who waited for professional crews to arrive during a peak demand period. A major technical concern in these scenarios is the wicking effect, where moisture travels upward through porous materials like insulation and drywall. Even if the floor appears dry, water trapped behind the baseboards can create a hidden environment where fungi flourish in the darkness. Using moisture meters and infrared cameras became a standard practice for savvy residents to ensure that the internal framing of the house reached an acceptable level of dryness before any cosmetic repairs were initiated. This thorough approach prevented the common mistake of sealing moisture into the walls.

Proactive steps taken by informed property owners proved that a comprehensive approach to risk management was the most effective way to handle the evolving threats of 2026. Rather than relying on outdated assumptions, successful individuals consulted with independent agents to perform a line-by-line audit of their existing policies to identify hidden exclusions. They integrated smart technology by installing Wi-Fi-enabled leak detectors near water heaters and sump pumps, which provided real-time alerts to smartphones the moment moisture was detected. These technological safeguards, combined with the purchase of specific flood and sewer endorsements, created a multi-layered defense strategy that functioned even when the residents were away from home. Moving forward, the most resilient households established a relationship with a certified restoration professional before an emergency occurred, ensuring they were prioritized during city-wide events. This strategic preparation turned a potential financial catastrophe into a manageable inconvenience that preserved both property value and peace of mind.