A fundamental disconnect has emerged between the fluid, instant-on nature of modern digital life and the rigid, often cumbersome processes of traditional insurance, creating a significant opportunity for disruption. Within the specialty insurance market, particularly travel, this gap is being aggressively closed by a new wave of digital-first Managing General Agents (MGAs) who are completely re-engineering the insurance lifecycle. Driven by the non-negotiable expectations of Millennial and Gen Z consumers, this transformation is moving the industry away from legacy models and toward a future defined by flexibility, simplicity, and a seamless, on-demand service delivery. It is a response not just to new technology, but to a profound cultural shift in how consumers interact with services, demanding control and transparency at every turn. The success of these emerging models indicates that for specialty insurance to remain relevant, it must evolve beyond being a static product and become a dynamic, integrated part of the customer’s digital experience.

A Customer-Centric Revolution

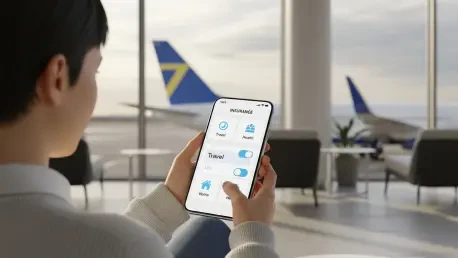

Engineering for the Digital Native

The driving force behind the market’s reshaping is the need to cater to the unique expectations of Millennial and Gen Z customers, a demographic that demands engagement and flexibility mirroring their experiences with other digital services. According to Ernesto Suarez, a veteran of the insurance industry, this generation has little patience for the friction inherent in traditional insurance products—any step in the customer journey that is clunky, slow, or confusing. To address this, digital-first MGAs are pioneering mobile-centric solutions that align with how younger consumers already manage their finances, travel, and other essential services. This includes introducing features that are rapidly becoming new industry standards, such as app-based policy management that gives customers complete control over their policies and the ability to make real-time adjustments, like pausing or modifying coverage on the fly. These innovations are not mere novelties; they represent a necessary alignment with established consumer behavior in an increasingly digital-first world, transforming insurance from a passive purchase into an active, manageable service.

The primary arena for this innovation has been travel insurance, an inherently complex product that is ideal for personalization but also highly susceptible to poor user experiences. By focusing on mobile-first design, innovators are giving customers unprecedented control and turning a once-static product into a dynamic tool. This approach is not just about convenience; it is a strategic move to build trust and demonstrate value in a language that digital natives understand. When a customer can effortlessly adjust their travel coverage from their smartphone just as easily as they can change a flight or book a hotel, the insurance product becomes an integrated and valued part of their journey rather than a begrudgingly purchased afterthought. This shift in control empowers the consumer and fundamentally alters the relationship between the insurer and the insured, fostering a sense of partnership and reliability that traditional models often lack, thereby setting a new benchmark for the entire specialty insurance sector.

Delivering Instant Value with Parametric Payouts

Among the most impactful innovations reshaping the customer experience is the wider adoption of parametric payouts, which has been instrumental in aligning insurance with the demand for immediate gratification. This model leverages automated, trigger-based claims for specific, verifiable events, such as a flight delay that exceeds a predetermined length of time. Once the trigger event is confirmed through a reliable data feed, the claim is automatically processed and paid without the customer needing to submit extensive paperwork or endure a lengthy review process. This functionality effectively eliminates the traditional, often adversarial, claims submission cycle, delivering near-instantaneous financial value at the precise moment of need. By turning a moment of travel frustration into a seamless and positive brand interaction, parametric insurance does more than just settle a claim; it actively builds customer loyalty and demonstrates the tangible benefit of the insurance product in a powerful, memorable way.

The strategic importance of parametric models extends far beyond just speed and efficiency; it represents a fundamental shift in the insurance value proposition from a reactive promise to a proactive service. This model builds a powerful foundation of trust by providing transparent, objective, and rapid resolutions. In a market where brand reputation is increasingly shaped by online reviews and real-time customer feedback, the ability to deliver on a policy’s promise instantly is a significant competitive differentiator. This proactive approach is resetting industry expectations for what a claims experience should be, moving the benchmark from a response time of several business days—now perceived as an eternity by modern consumers—to one of minutes or hours. As this technology becomes more sophisticated and widely applied, it will continue to push the entire specialty market toward a new standard where immediate, automated support is not a luxury feature but a core component of the product itself.

Redefining the Core Insurance Process

Transforming the Moment of Truth in Claims

The claims process has long been identified as the most critical touchpoint in the insurance relationship and, historically, the area where traditional propositions have most often failed the customer. Suarez describes the customer’s “worst nightmare” as the experience of being repeatedly handed off between different providers within a long and disjointed value chain, a common problem when policies are sold through partners or aggregators. This fragmented approach creates confusion, delays, and immense frustration at a time when the customer is already under stress. The failure to provide a cohesive, supportive, and simple claims experience is a primary driver of customer dissatisfaction and brand erosion. Recognizing this, innovative MGAs are tackling this problem head-on by leveraging technology to shorten and fundamentally simplify this chain, ensuring the “moment of truth” becomes a positive reflection of the insurer’s promise rather than a source of further distress for the policyholder.

The solution to the fragmented claims experience lies in centralizing servicing and automating workflows to create a single, cohesive, and less stressful journey for the customer. By taking ownership of the entire process, even when policies are distributed through partners, modern insurers can eliminate the frustrating handoffs that plague legacy systems. While sophisticated automation is key to achieving the speed and efficiency that customers now demand, these systems must also be designed to be adaptive. Customers will consistently present new and unexpected problems, and the technology must be flexible enough to handle exceptions and escalate complex cases to human agents seamlessly. This combination of powerful automation and intelligent human oversight is critical to meeting and exceeding modern expectations. The industry standard is shifting rapidly; a response time of five business days is no longer acceptable. Today’s customers expect immediate contact after filing a claim, and the industry’s innovators are building their entire operational models around delivering that immediacy.

The Strategic Advantage of Pre-Underwriting

A pivotal yet often overlooked strategy powering this new generation of insurance products is the disciplined application of pre-underwriting. This proactive approach involves creating a “strong rule set” and rigorous underwriting criteria at the very inception of the product, long before it ever reaches the market. By clearly defining the risks being covered and the conditions for a claim, insurers can build efficiency and clarity into the system from the ground up. This methodical approach has a cascading positive effect that permeates the entire customer lifecycle. First and foremost, it naturally leads to the creation of simpler, more understandable products. When the rules are clear internally, the policy language presented to the customer can be more straightforward, reducing ambiguity and helping consumers make more informed purchasing decisions. This foundation of clarity is essential for building trust and setting accurate expectations from the outset of the insurance relationship.

The benefits of a strong pre-underwriting framework extend far beyond product simplicity, directly enabling a faster and more efficient process that flows seamlessly from the point of sale through to the final claim settlement. With a clear and robust rule set in place, insurers can automate a greater portion of the claims validation and payment process with confidence, as the system has already been designed to handle the vast majority of scenarios. This reduces the need for manual intervention, minimizes the potential for disputes, and accelerates resolution times dramatically. This strategic foresight is a key differentiator separating market innovators from incumbents, as it demonstrates a holistic understanding of the insurance lifecycle. Instead of merely retrofitting new technology onto outdated processes, these companies are re-architecting their entire operational model around a core of discipline and clarity, ensuring a superior experience for both the customer and the insurer.

The New Ecosystem of Distribution and Innovation

The Rise of Embedded and On-Demand Sales

A structural shift in how insurance is sold and distributed is well underway, marked by the rapid expansion of embedded travel coverage. This model involves offering insurance not as a standalone product but as an integrated, optional add-on within the booking process for flights, hotels, or car rentals. This allows insurers to meet consumers precisely at their moment of need with a product that is highly relevant and tailored to a specific, identifiable risk. Suarez views this as more than a mere channel strategy; he defines it as a “whole different way” of positioning and selling insurance. It fundamentally changes the sales dynamic by seamlessly integrating an insurance product into a purchase that was not primarily about insurance, thereby removing the friction of a separate and often cumbersome buying journey. The customer is presented with a simple, contextual offer that they can accept with a single click, transforming the acquisition process into an effortless and intuitive experience.

This powerful trend of embedding insurance at the point of need is quickly expanding beyond the travel sector and into other retail specialty lines, as providers seek to align their coverage with specific customer behaviors and life events. The success of the model in travel has provided a clear blueprint for its application in areas such as gadget insurance offered at the point of electronic purchase, short-term motor policies available through car-sharing apps, and pet insurance presented during veterinary appointments or at animal shelters. This expansion reflects a broader market recognition that insurance is most valuable when it is accessible and contextually relevant. By moving away from a product-centric sales approach and toward a customer-centric distribution model, insurers can more effectively demonstrate their value proposition and integrate their services into the fabric of their customers’ daily lives, making protection a natural extension of their activities rather than a separate, complex decision.

Brokers and MGAs as a Driving Force

Despite the powerful move toward direct and digital channels, the role of insurance intermediaries is not diminishing; on the contrary, it is becoming more vital than ever. The article strongly affirms that brokers and MGAs are now the primary drivers of innovation across the specialty insurance sector. With their inherent agility and deep market knowledge, they are adeptly “filling gaps that were not really addressed by insurers.” Traditional carriers, often encumbered by legacy systems and a more cautious approach to change, can be slow to adapt. In contrast, brokers and MGAs can move quickly to identify emerging customer needs and leverage new technologies to develop the “more interesting propositions” that are defining the future of the market. They act as a crucial bridge between the large-scale capacity of underwriters and the specific, evolving demands of modern consumers, making them an indispensable part of the insurance ecosystem.

A key development powering this innovation is the increasing collaboration between MGAs, which excel at product design and distribution, and specialized insurtech enablers that provide the underlying technology platforms. This synergistic partnership allows each party to focus on its core strengths, resulting in the rapid development and deployment of sophisticated, customer-centric insurance products. This model is attracting significant attention and investment from the wider industry, which recognizes its potential to accelerate transformation. Furthermore, in this digital-first landscape, the influence of online platforms on consumer trust cannot be overstated. Online review sites have become powerful “gatekeepers of visibility and trust,” with Suarez noting that they “sit at the heart of any strategy.” A provider’s digital reputation, amplified and scrutinized by AI-driven search algorithms, is now a foundational element of its brand and a critical factor in its ability to attract and retain customers in a transparent and highly competitive marketplace.

A New Standard for Service and Trust

The transformation of the specialty insurance market ultimately reset fundamental expectations around service, responsiveness, and trust. The claims turnaround time, once measured in days or weeks, emerged as a key performance indicator by which all providers were judged. For the modern customer, a response time of five business days was perceived as a lifetime and was no longer an acceptable standard of service. The industry learned that to maintain its relevance, particularly in the dynamic travel sector, the entire experience had to be as smooth and intuitive on a mobile screen as it was on a desktop. This required more than just the adoption of new technology; it demanded a deep cultural shift toward prioritizing simplicity and building trust at every single stage of the product lifecycle, from initial purchase to final claim settlement. The innovations pioneered in this space demonstrated that claims could be resolved with the same speed and efficiency with which they were triggered, establishing a new benchmark for the entire industry.