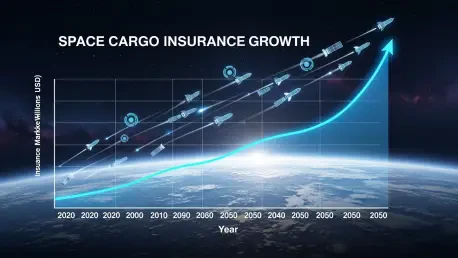

The space industry is soaring into uncharted territory, and as it expands, the need for specialized insurance to shield against the astronomical risks of satellite launches, cargo transport, and deep-space missions has never been more critical. Starting from a market value of USD 2.35 billion in 2025, projections indicate a staggering climb to USD 5.0 billion by 2035, driven by a robust compound annual growth rate (CAGR) of 7.8%. This growth isn’t just a statistic—it mirrors the escalating stakes of an industry where a single mishap can result in losses worth hundreds of millions of dollars. From powering global communication networks with satellites to private companies venturing into space tourism, the financial exposure tied to these endeavors is immense. Space cargo insurance, once a niche segment, is rapidly evolving into a cornerstone of risk management, ensuring that both commercial and governmental players can innovate and explore with a safety net in place. As the next decade unfolds, this market promises to transform, fueled by technological breakthroughs and an ever-expanding scope of space activities.

Fueling the Surge: Key Market Drivers

The momentum behind the expansion of space cargo insurance is largely propelled by an unprecedented increase in satellite launches and the accelerating privatization of space endeavors. Commercial entities and government bodies alike are deploying satellites at a remarkable rate to support broadband internet, navigation systems, and earth observation initiatives. Each of these launches carries inherent risks, from catastrophic failures during ascent to malfunctions in orbit, necessitating robust insurance coverage to protect against financial ruin. Moreover, ambitious exploration missions targeting the Moon, Mars, and beyond are introducing new layers of complexity and risk, further driving the demand for specialized policies that can address the unique challenges of deep-space ventures. This surge in activity underscores the critical role of insurance as a safeguard for high-value investments in an industry where the margin for error is razor-thin.

Beyond the sheer volume of launches, the privatization of space activities is reshaping the insurance landscape in profound ways. Companies leading the charge in space innovation are not only launching satellites but also pioneering new frontiers like cargo transport to low Earth orbit and space tourism. These ventures introduce novel risks that traditional insurance models are often ill-equipped to handle, creating a pressing need for tailored solutions. As private players take on more ambitious projects, the financial stakes climb higher, amplifying the importance of comprehensive coverage that can mitigate losses from launch failures, in-orbit damages, or third-party liabilities. This dynamic environment is pushing insurers to adapt quickly, developing products that align with the specific needs of a rapidly evolving sector while ensuring that the growing number of stakeholders can operate with confidence in an inherently unpredictable field.

Revolutionizing Risk: The Role of Technology

Technological advancements are fundamentally transforming the space cargo insurance market, making it more precise and accessible to a wider range of participants. The integration of artificial intelligence (AI) and big data analytics into risk assessment processes is enabling insurers to predict potential issues with unprecedented accuracy, even in an industry historically hampered by a lack of comprehensive loss data. These tools allow for the creation of detailed risk profiles for each mission, refining pricing models and reducing premium costs that have long been a barrier to entry. As a result, smaller companies and emerging players can now secure the coverage they need to compete, fostering greater innovation and participation in the space sector. This technological shift is proving to be a game-changer, reshaping how insurers approach a field defined by high stakes and uncertainty.

In addition to AI and analytics, improvements in satellite monitoring are providing real-time insights that further enhance risk management capabilities. Insurers can now track assets in orbit with greater precision, identifying potential issues before they escalate into costly failures. This capability not only reduces the likelihood of claims but also builds trust between insurers and clients by demonstrating a proactive approach to risk mitigation. Furthermore, the adoption of these technologies is encouraging the development of customized policies that cater to the specific phases of a mission, whether it’s the high-risk launch stage or the ongoing challenges of in-orbit operations. As technology continues to evolve, it is expected to drive down costs and improve accessibility, ensuring that space cargo insurance keeps pace with the rapid advancements of the industry it serves over the coming decade.

Navigating Obstacles: Challenges in the Market

Even with a promising growth trajectory, the space cargo insurance market faces significant hurdles that must be addressed to sustain its upward momentum. The most prominent challenge lies in the prohibitively high cost of premiums, a direct reflection of the immense value tied to space assets. A single satellite or launch vehicle can represent an investment of hundreds of millions of dollars, and the potential for total loss during a mission necessitates extensive coverage that drives up costs. For many smaller companies or emerging players, these premiums can be a substantial barrier, limiting their ability to participate in the space economy. Addressing this issue will require innovative approaches to pricing and risk-sharing mechanisms that can make insurance more affordable without compromising the protection it offers.

Another pressing obstacle is the scarcity of historical loss data, which complicates the ability of insurers to accurately predict and price risks. Unlike more established industries, the space sector lacks a deep reservoir of empirical evidence due to the relatively low number of missions and incidents over time. This forces insurers to rely heavily on theoretical models, introducing a level of uncertainty that can affect policy design and premium calculations. Overcoming this challenge will depend on improved data collection efforts and collaboration across the industry to build a more robust dataset. As more missions are launched and tracked over the next decade, the accumulation of real-world information will likely enhance risk modeling, paving the way for more precise and cost-effective insurance solutions that benefit all stakeholders.

Global Dynamics: Market Segments and Regional Trends

The space cargo insurance market is characterized by a complex array of segments that cater to diverse needs across the industry. Coverage types are broadly categorized into launch insurance, which protects against failures during the critical ascent phase, in-orbit insurance for assets operating in space, and third-party liability insurance to address damages caused to external parties. End users span commercial space companies, increasingly dominant due to private investments in satellite constellations and tourism, as well as government and defense agencies with significant space programs. This segmentation highlights the varied risks and requirements within the sector, necessitating a flexible approach from insurers to meet the specific demands of each mission or client, ensuring comprehensive protection across all phases of space operations.

Geographically, the market showcases distinct regional trends that reflect varying levels of investment and technological advancement. North America stands at the forefront, driven by the presence of major space agencies and private industry leaders in the United States and Canada, which account for a substantial share of global launches and missions. Europe follows closely, with countries like Germany, France, and the UK contributing through advanced satellite manufacturing and launch capabilities. Meanwhile, the Asia-Pacific region is rapidly gaining ground, fueled by ambitious space programs in China, India, and Japan, which are investing heavily in technology and infrastructure. Emerging markets in South America and the Middle East and Africa are also beginning to make their mark, albeit on a smaller scale, signaling a broadening global interest in space activities and the accompanying need for tailored insurance solutions.

Uncharted Territories: Future Opportunities

As the space industry pushes boundaries, new opportunities are emerging for insurers to carve out innovative niches within the cargo insurance market. Space tourism, once a distant vision, is becoming a tangible reality, with private companies preparing to ferry passengers into orbit and beyond. This development opens a fresh frontier for insurance products that can cover not only cargo but also human lives, addressing risks unique to this nascent sector. Insurers who can develop policies tailored to the safety and liability concerns of space tourism stand to gain a significant foothold in a market poised for explosive growth. This evolving landscape presents a chance to pioneer coverage options that could redefine how risk is managed in commercial space travel over the coming years.

Simultaneously, the ongoing privatization of space is fostering partnerships between insurers and private entities, creating avenues for customized solutions that align with specific mission objectives. The demand for bespoke policies—those designed to cover particular risks or stages of a mission—is on the rise, reflecting the diverse needs of an industry in flux. Additionally, as exploration missions to distant celestial bodies increase, insurers have the opportunity to craft specialized products for these high-risk endeavors, addressing challenges that differ vastly from traditional satellite launches. By forging strategic alliances and leveraging technological advancements, insurers can position themselves at the forefront of this transformative decade, capitalizing on the expanding scope of space activities to deliver value and security to a growing array of stakeholders.

Building Resilience: Reflecting on the Path Ahead

Looking back over the discussions, it becomes evident that the space cargo insurance market has carved out a pivotal role in supporting an industry defined by innovation and risk. The projected growth from USD 2.35 billion in 2025 to USD 5.0 billion by 2035, with a steady CAGR of 7.8%, highlights the increasing dependence on insurance to protect against the financial perils of space missions. Challenges such as high premiums and limited data have posed significant barriers, yet the integration of technology and the rise of new sectors like space tourism offer pathways to overcome them. Moving forward, stakeholders must prioritize collaboration to enhance data collection and refine risk models, ensuring that insurance remains both accessible and effective. Additionally, insurers should focus on developing flexible, innovative products that cater to emerging needs, from deep-space exploration to passenger travel. By adapting to the dynamic nature of the space sector, the insurance industry can solidify its position as a vital enabler of progress, safeguarding investments and fostering confidence in humanity’s extraterrestrial ambitions.